Message: Return type of CI_Session_files_driver::open($save_path, $name) should either be compatible with SessionHandlerInterface::open(string $path, string $name): bool, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Return type of CI_Session_files_driver::close() should either be compatible with SessionHandlerInterface::close(): bool, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Return type of CI_Session_files_driver::read($session_id) should either be compatible with SessionHandlerInterface::read(string $id): string|false, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Return type of CI_Session_files_driver::write($session_id, $session_data) should either be compatible with SessionHandlerInterface::write(string $id, string $data): bool, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Return type of CI_Session_files_driver::destroy($session_id) should either be compatible with SessionHandlerInterface::destroy(string $id): bool, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Return type of CI_Session_files_driver::gc($maxlifetime) should either be compatible with SessionHandlerInterface::gc(int $max_lifetime): int|false, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Cannot modify header information - headers already sent by (output started at /home2/franchi4/public_html/legal/system/core/Exceptions.php:271)

Thought GST is exceptionally celebrated for the free stream of credit, there are no less than twelve situations where input charge credit isn't accessible to the citizen under GST administration. As stated, Input assess credit (ITC) under GST is essential to comprehend, in light of the fact that it is specifically identified with your GST impose installment, thus any slip-up may bring about fines and punishments.

Before talking about the 12 cases, let us comprehend the importance of Input assess credit.

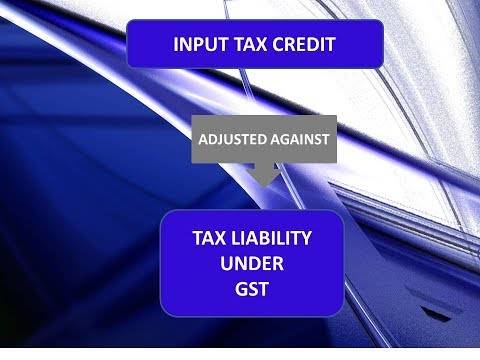

2.0 Meaning of Input Tax Credit (ITC) under GST

According to condition 63 of segment 2 of CGST, input charge credit implies the credit of info impose.

The info impose implies the focal assessment (CGST), state Tax (SGST), coordinated expense (IGST) or Union domain assess (UTGST) charged on any supply got or bought by an enrolled assessable individual on products or administrations or both.

Case: Suppose you purchase a crude material from Kerala. Your seller in Kerala will now charge IGST to you. Subsequently, that IGST should be your info impose.

Give us now a chance to advance and see all the 12 situations where credit under GST isn't permitted to be set off.

#Case no.1 – Input assess credit (ITC) of Motor vehicles and other transport not permitted under GST

According to GST law, the ITC on engine vehicles paid should not be permitted to set off against yield impose obligation. In another word, you can't guarantee the credit on engine vehicles and other transport.

Case: Suppose you purchase an auto for your business. According to engine vehicle act, the auto is secured under the meaning of engine vehicle, consequently ITC on auto might not be permitted.

Situations where Input Tax Credit (ITC) might be accessible on engine vehicle under GST

There are just four situations where ITC on engine vehicles are permitted under GST. The four cases are as per the following:

Merchant of engine vehicles: If you are a dealer of an engine vehicle, at that point ITC on autos acquired might be permitted.

Case: If you are an enrolled merchant of Maruti autos and you acquired 10 autos for Rs.50 lakh in a